Getting Your Money in Order

So this is Stuart Wills here, and I just wanted to talk to you about getting your money in order.

It’s something that most of us need to do from time to time, and it’s great that you’re having a look at this video to give you some idea of where to get started.

Let’s Get Started – Getting Your Money in Order

What are the first steps?

Firstly, you need to establish a starting point.

With any plan, unless you know where you’re starting from. It’s really, really hard to know where you’re going if you have not worked out where you are starting – the starting point.

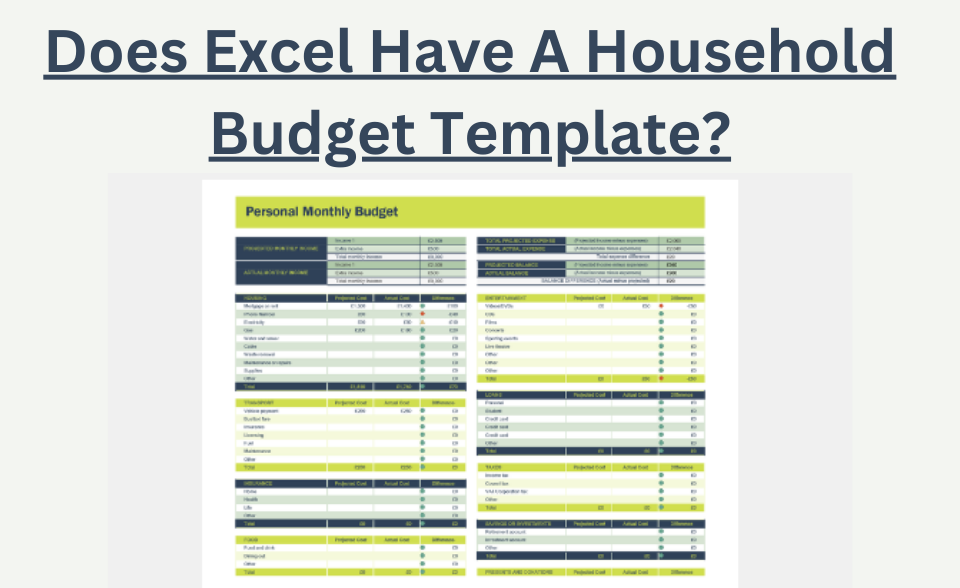

So the first thing we’d suggest you do is look at downloading your bank statements and then coding and entering those expenses into a good spreadsheet.

Now the spreadsheet that we use is Budget Planner and in this video I explain a bit more about the way that we suggest that you get your money in order too.

Why We Suggest Budget Planner

The reason we use this is it’s very, very simple to enter stuff in, and it also reports really, really well on a dashboard, so you can get a really good idea of your total financial position, including your income and expenses.

Now when you do this, you may find that things don’t look great, but it’s really important to remember that this is a starting point, it’s not the end point.

The whole idea is to get a realistic starting point, review your spending, and look particularly for any bad spending.

Plug The Leaks!

Once you’ve got the information entered then you need to do is start looking at plugging the leaks.

It doesn’t matter how big a ship is or how big the hole is – if it’s leaking it will sink.

And that’s the same in your situation.

So what we need to do is we need to plug those leaks, and you need to do it now.

It’s no use procrastinating, those leaks are not going to stop by themselves.

Of course, once you have found those leaks and identified where you can save on spending, then you have some additional money in your budget, and you need to look at what you can do with it.

Generally speaking, there’s three things you can do with it.

You can either pay debt, you can put it into some form of savings, or you can invest it and often you’ll try to do a little bit of each.

Paying Off Debt

Now paying debt is always good, as it gives immediate financial reward, because you’re going to save on the interest that you’re paying for that debt.

Even paying off an interest free loan helps as that means you lower your outgoings (the repayments) which frees up more money to be saved or invested.

Start Saving, or Saving More

It’s also good to have some savings.

This means that you have a back-stop where you can access your own money should something happen, and therefore you don’t need to dive into debt again.

It maybe that you need to use your savings to fix the car, go to the dentist, shift houses etc. There are always those unexpected costs that tend to pop up when you can least afford them. There are hard to budget for, but you know that they will come up from time to time and therefore your savings means you can afford these.

There are a number of bank accounts that you can use for your savings, and generally we suggest that you have a small savings account with your main bank, but then also have some savings with another bank.

Let’s Start Investing Too…

Of course investing is always good, and it’s not the same as savings.

This is a mistake that so many people make.

The idea of savings is to have something for that rainy day, to cover those unexpected expenses, or to save for something like a holiday, a wedding, or deposit for a home. Those are all short-term goals, being probably less than three years.

When we talk about investing, what we’re talking about there is generating income over the long term.

Your Investment Options

There are literally thousands of investment options that you can use, but I’m going to cover just four here.

KiwiSaver – this is an investment for your retirement, however you can normally withdraw for your first home as well. KiwiSaver is now the main New Zealand retirement scheme. It started in 2007 and so is still quite young, and although it’s not compulsory employers are required to match contributions to 3% and also the Government contribute a ‘tax credit” as well. This makes Kiwisaver a popular option, but you still should make an informed decision on what provider and fund you invest in.

Investing in shares – this is where technically you’re investing a small amount in a company, and getting paid a dividend plus hopefully the shares will increase in value over time. If you have a large amount of cash to invest then you might want to speak with a financial planner, but many Kiwis are more into the DYI and using an App like Sharesies. This is an easy way to invest and is something that I personally do, investing in a few companies and funds including one of my favorites: Berkshire Hathaway.

Crypto (Investing in Mining) – this is one of my favorite investments. It’s not just investing in the hope that the cryptocurrency is going to increase in value, it’s actually investing in the mining of crypto and then you can hold onto the cryptocurrency as an investment or my preference which is to invest into a “pool” that operates as a “rise only market” which is a safe way to invest. I purchased Mining Software through BeepX with an upfront cost of USD$199.95 and then USD$50 monthly.

These are three ways that I use to invest.

Get Your Budget Planner

The next thing we need to do is make sure that you have the full budget manager, and you use it.

You need to put in your calendar to be looking at that either every day or every week, updating it and adjusting it so that you have a true financial position in front of you all of the time.

If you remember we talked about the starting point, identifying where you are today and what you want to be doing. With the dashboard on the Budget Planner you can see exactly where you are today and every day in the future.

Have a look at how to set up your Budget Planner as this also will give you an idea of what to expect.

I hope you found this helpful, and I really hope over the next weeks and months you use this to its fullest extent.